Meta Title: Reinstatement Cost Assessment for Insurance 2026 | South London Guide

Meta Description: Is your South London home underinsured? Discover how a RICS-certified reinstatement cost assessment for insurance protects your property from financial disaster in 2026.

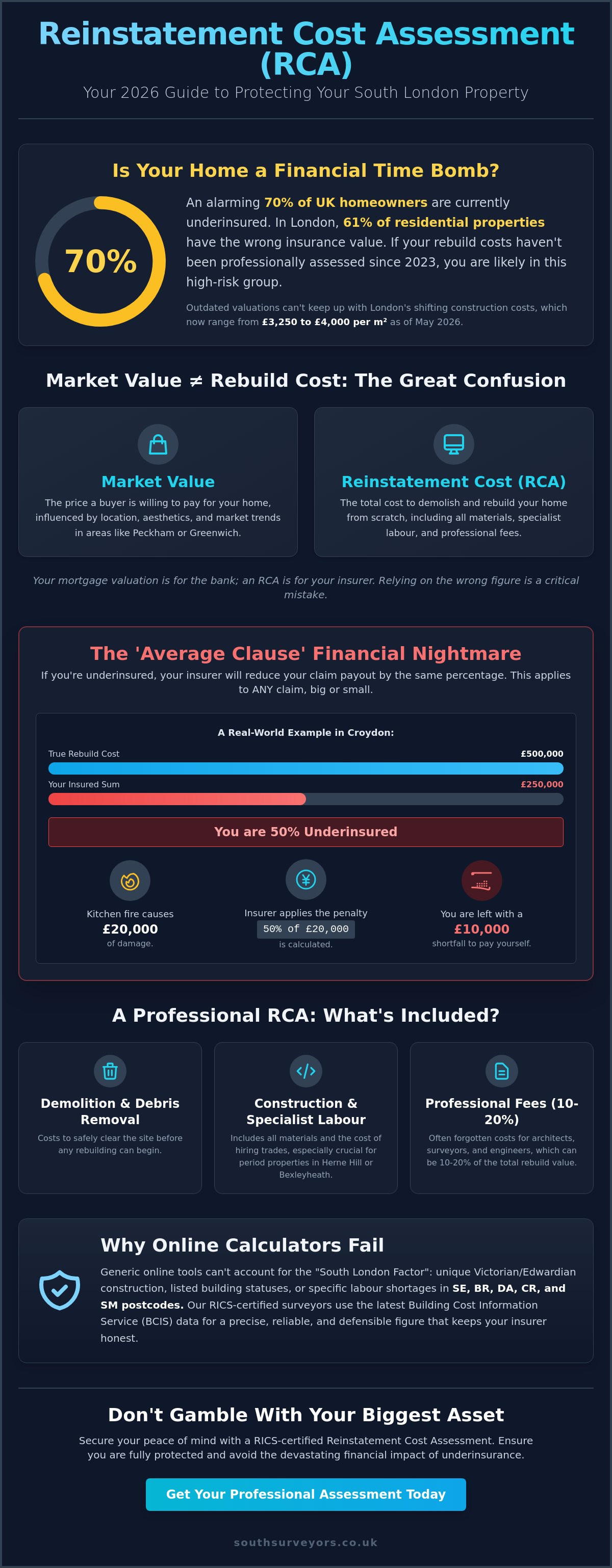

What if your insurance company is quietly betting against you? You already know the property market in spots like Peckham and Dulwich is a wild ride, but you probably assume your buildings insurance has your back if the worst happens. However, with London construction costs shifting faster than a pop-up gallery’s opening night, there is a high chance your current policy is based on a total fiction. If you haven’t looked at your rebuild figures since 2023, you’re likely part of the 70% of UK homeowners currently facing a massive insurance gap.

Discovering that your insurance might be “lying” to you is a wake-up call, but a professional reinstatement cost assessment for insurance is the ultimate antidote to that uncertainty. We understand you want total clarity without the corporate fluff, which is why we’ve put together this guide to help you navigate the 2026 landscape. We’ll show you how to avoid the dreaded “Average Clause” and ensure your Victorian terrace or modern apartment in the SE, BR, or DA postcodes is covered for every single brick, beam, and bespoke finish.

Key Takeaways

- Understand why a professional reinstatement cost assessment for insurance is the only way to calculate your home’s true rebuild value, including often-forgotten costs like debris removal and architect fees.

- Decode the “Average Clause” to see how being even slightly under-insured can lead to a massive financial shortfall when you try to make a claim.

- Learn why South London’s period homes in areas like Herne Hill and Greenwich require a bespoke approach due to their unique construction and potential listing status.

- Discover the step-by-step process our RICS-certified experts use to provide you with a precise, reliable figure that keeps your insurance provider honest.

What on Earth is a Reinstatement Cost Assessment (RCA)?

Let’s clear something up right away: your home’s market value is what a trendy buyer might pay for your pad in Peckham. A reinstatement cost assessment for insurance is a completely different beast. It is a professional, RICS-certified calculation of exactly what it would cost to rebuild your home from the ground up if the unthinkable happened. It isn’t just about the bricks and mortar; it’s a comprehensive figure that includes everything from demolition and debris removal to the professional fees for architects, surveyors, and engineers. In 2026, these professional fees alone typically represent 10% to 20% of your total rebuild cost.

Relying on an assessment from three years ago is a dangerous game. As of May 2026, construction costs in London have shifted significantly, with new build rates now sitting between £3,250 and £4,000 per square metre. If you haven’t updated your figures recently, you could be facing the financial nightmare of under-insurance. With 61% of London residential properties currently insured for the wrong amount, getting a precise figure isn’t just “good practice,” it’s vital for your financial survival.

Market Value vs. Rebuild Cost: The Great Confusion

It’s easy to get these two numbers mixed up. A tiny, one-bedroom flat in Greenwich might have a sky-high market value because of its proximity to the park and the Cutty Sark, yet its rebuild cost might be relatively modest. On the flip side, a sprawling Edwardian home in Bromley or a property with bespoke Bexleyheath stonework could cost far more to rebuild than its current sale price. This is why using your mortgage valuation as a guide for your insurance premium is a massive mistake. Your bank cares about what the house is worth on the open market; your insurer only cares about the cost of the skip hire, the scaffolding, and the specialist labor required to put it back together.

Why ‘Rough Guesses’ Don’t Cut it Anymore

In 2026, the “finger in the wind” approach to insurance is dead. Labor shortages across the SE and CR postcodes have pushed trade wages higher, meaning a “rough guess” from an online calculator won’t reflect the reality of hiring a specialist bricklayer in Croydon or a carpenter in South East London. Our RICS-certified surveyors don’t guess. We use the latest Building Cost Information Service (BCIS) data to ensure every pound is accounted for. A professional reinstatement cost assessment for insurance is a standalone protection that ensures you aren’t paying for cover you don’t need, or worse, left with a massive bill when you need to claim.

The ‘Average Clause’: Why Under-Insurance is a Financial Nightmare

Insurance companies aren’t exactly known for their charitable nature. If you’ve under-egged your rebuild costs to save a few quid on your monthly premium, you’re walking straight into the “Average Clause” trap. This clause is the insurance industry’s way of penalizing homeowners who haven’t done their homework. It’s a simple, brutal rule: if you’re under-insured by a certain percentage, your insurer will reduce any claim payout by that exact same percentage. It doesn’t matter if you’re claiming for a total rebuild or a minor mishap; the penalty applies across the board.

Let’s look at a real-world disaster in Croydon. Imagine a kitchen fire causes £20,000 worth of damage. You might think you’re safe because your total policy limit is much higher than that. However, if your reinstatement cost assessment for insurance shows your home actually costs £500,000 to rebuild, but you only insured it for £250,000, you’re 50% under-insured. The insurer will only pay out 50% of your fire claim. That £20,000 repair job just became a £10,000 bill out of your own pocket. In 2026, insurers are becoming even stricter with these assessments to manage their own risks and comply with updated FCA Consumer Duty regulations.

The Math Behind the Disaster

The ‘Average Clause’ formula is calculated as: (Sum Insured ÷ True Rebuild Cost) x Amount of Claim = Total Payout. Consider a semi-detached house in Sutton (SM) that would cost £600,000 to rebuild today. If the homeowner relies on an outdated figure of £400,000, they are only covered for two-thirds of the value. If a storm rips £15,000 worth of tiles off the roof, the insurer will only hand over £10,000. The “hidden” loss of £5,000 is a high price to pay for skipping a professional survey. The Association of British Insurers (ABI) provides excellent guidance on securing your property, but they are very clear: the responsibility for the rebuild figure sits squarely on your shoulders.

Avoiding the ‘Negligence’ Trap

Getting an accurate reinstatement cost assessment for insurance isn’t just about the payout; it’s about legal protection. When you provide a RICS-certified figure, you’re effectively removing the insurer’s ability to argue that you were negligent in your valuation. Establishing a professional RICS valuation as a baseline ensures you aren’t just guessing. On the flip side, being over-insured is a total waste of cash. There is no point paying inflated premiums for a £1 million rebuild if your Bromley home only costs £700,000 to put back together. That extra money is much better spent on a flat white and a pastry in a Blackheath café. If you’re unsure where your current policy stands, you can always chat with our team for a quick bit of local advice.

How We Calculate Your Home’s True Rebuild Value

Getting a reinstatement cost assessment for insurance isn’t just about a surveyor wandering around with a clipboard and a tape measure. It is a meticulous, five step process designed to give you total clarity. First, we measure the Gross Internal Area (GIA). We don’t just pace out the rooms; we calculate the total floor area inside the external walls, including every nook and cranny of your property. In tight South East London postcodes, every square centimetre counts when construction rates are sitting between £3,250 and £4,000 per square metre in 2026.

Next, we look at what your home is actually made of. While standard bricks are common, many homes in the DA postcode feature bespoke Bexleyheath stonework or unique masonry that requires specialist trades. We then factor in “External Works.” People often forget that their insurance needs to cover more than just the house itself. We include the cost of rebuilding garden walls, driveways, and even that high end patio in Dulwich. Finally, we add a contingency for professional fees. In 2026, you should expect architects, surveyors, and engineers to account for 10% to 20% of the total cost, plus the inevitable 20% VAT on top of the rebuild figure.

What We Look for During the Visit

During the site inspection, we hunt for the details that online calculators miss. We check for original sash windows, period fireplaces, and decorative plasterwork that would be incredibly expensive to replicate. Site access is another huge factor. If your home is on a narrow street in the SE postcode where getting a crane or a skip is a logistical nightmare, your rebuild costs will naturally be higher. We also identify potential “hidden” costs, such as hazardous materials like asbestos, which can significantly inflate demolition and debris removal expenses before the first new brick is even laid.

The Final Report: Clarity and Confidence

Once the data is crunched using current 2026 regional cost indices, you receive a comprehensive document. This is exactly what your insurance broker needs to see to set your premiums accurately. It provides a precise figure that eliminates the guesswork and protects you from the “Average Clause” we discussed earlier. We recommend updating your RCA every three years, with annual desktop reviews to keep pace with the 3% to 4% inflation rates we are seeing this year. If you want to dive deeper into how these inspections work, it is worth understanding your RICS home survey and how it differs from a standard valuation. A professional reinstatement cost assessment for insurance is about more than just numbers; it’s about ensuring your South London home is truly protected.

Period Properties and Posh Postcodes: The South London Factor

South London is a patchwork of architectural history, but that charm comes with a hefty price tag if you ever need to rebuild. In neighborhoods like Herne Hill, the cost of recreating an Edwardian semi-detached is far higher than a modern equivalent. If your property is Grade II listed, particularly in historic pockets of Greenwich, you need a specialized reinstatement cost assessment for insurance. Listed status means you can’t just slap on some modern bricks; you’ll need heritage-approved materials and specialist trades who know their way around 19th-century construction methods.

Navigating the logistics of the ‘South London Jungle’ means acknowledging that narrow access in SE postcodes often inflates costs. If a rebuild requires a crane but the property is tucked down a one-way street, the bill climbs fast. Even in Dartford (DA), where you might expect a bit of a price break compared to Central London, the 2026 labor shortage keeps specialist trade wages high. These regional nuances are why a generic insurance quote is a dangerous gamble.

The Victorian Terrace Challenge

Matching original materials like lime mortar, Welsh slate roofs, and decorative plasterwork is a specialist job. Modern ‘off-the-shelf’ insurance calculators fail these beautiful old homes because they assume standard modern materials and contemporary building speeds. We often find that a Level 3 building survey is the first red flag for a homeowner, revealing that their insurance figure hasn’t accounted for the sheer cost of heritage restoration. Relying on a basic policy for a period home is like trying to fix a Swiss watch with a sledgehammer; it simply won’t end well.

Post-Renovation: Did You Just Invalidate Your Policy?

Renovations are the silent killers of insurance policies. If you’ve just finished a loft conversion in Morden (SM) or a bifold-door kitchen extension, your previous reinstatement cost assessment for insurance is officially obsolete. You’ve increased the footprint and the quality of the finish, meaning the ‘sum insured’ on your policy no longer covers the full reality of your home. If the builders have just packed up their tools, your next phone call shouldn’t be to a decorator, but to a surveyor to ensure you haven’t accidentally invalidated your cover. Don’t leave your most valuable asset to chance; book your professional RCA with South Surveyors today to get your figures exactly right.

Securing Your Property with South Surveyors

Let’s be honest, faceless corporate robots are fine for ordering a late night pizza, but they shouldn’t be anywhere near your home’s insurance valuation. At South Surveyors, we pride ourselves on being your knowledgeable neighbors rather than just another name on a corporate spreadsheet. We live and work across the SE, BR, and CR postcodes, which means we understand the local property market from the inside out. Our RICS-certified expertise isn’t wrapped in impenetrable technical jargon; it’s delivered with the clarity and confidence you deserve. When you commission a reinstatement cost assessment for insurance from our team, you’re getting a report that is meticulous, easy to digest, and tailored specifically to your home’s unique character.

Why Local Expertise Matters

Local expertise is the secret sauce that prevents financial disaster. We know that a Victorian conversion in Eltham faces different rebuild challenges than a modern apartment in Peckham. In 2026, with labor shortages pushing trade wages higher across South London, having a surveyor who knows the local “boots on the ground” reality is vital. You won’t find yourself trapped in a never-ending call center loop here. You’ll speak directly to a human being, a professional surveyor who can walk you through the numbers and explain how we accounted for everything from South London’s narrow access issues to those 4% indexation rates. It’s this personal touch that provides the genuine peace of mind that comes from knowing your biggest asset is protected.

Your Next Steps to Total Protection

Securing your property doesn’t have to be a headache. The first step is to move from “hoping for the best” to knowing for sure. Start by gathering your current insurance documents and any recent building survey reports you’ve had commissioned. These documents help us build a comprehensive picture of your property’s history and current state. Whether you’re in a leafy suburb in Bromley or a bustling street in Croydon, we’ll help you determine if your current cover is actually fit for purpose. Remember, research from April 2026 shows that only 7% of UK properties are currently insured for the correct amount. Don’t let your home be part of the underinsured majority. Take the logical next step toward total protection and get a tailored Reinstatement Cost Assessment from South Surveyors today.

Take Control of Your Home’s Financial Future

You now know that your home’s market value is a world away from its actual rebuild cost. You also understand how the “Average Clause” can turn a small claim into a massive out of pocket expense. In the unpredictable construction market of 2026, a professional reinstatement cost assessment for insurance is the only way to ensure your property is shielded from the risk of underinsurance. Whether you own a Victorian gem in Dulwich or a modern family home in Sutton, precision is your best friend.

At South Surveyors, we are proud to be regulated by RICS and serve as the go to local experts for the SE, BR, DA, CR, and SM postcodes. With over 100+ five-star reviews from South London homeowners, we combine technical excellence with a personal touch that corporate firms just don’t match. Don’t leave your most valuable asset to chance. Get a professional Reinstatement Cost Assessment from South Surveyors today. It’s time to trade that lingering doubt for real confidence and peace of mind. Your home deserves nothing less.

Frequently Asked Questions

Is a Reinstatement Cost Assessment the same as a valuation?

No, these two figures serve completely different purposes. A valuation estimates what a buyer might pay for your home in Peckham or East Dulwich, whereas a reinstatement cost assessment for insurance calculates the total cost to rebuild the structure from scratch. The RCA includes “hidden” expenses like site clearance, debris removal, and professional fees that a standard market valuation ignores.

How often should I get an RCA for my South London home?

You should commission a full professional assessment every three years to stay protected. In the intervening years, it is sensible to perform annual desktop reviews to keep pace with the 3% to 4% construction inflation rates recorded in 2026. If you finish a major project, such as a kitchen extension in Bromley, you should update your figures immediately to avoid being underinsured.

Can I just use an online rebuild calculator instead?

Online calculators are a risky shortcut for South London’s unique property landscape. These tools often rely on national averages that don’t reflect the higher labor costs and trade shortages currently impacting the CR and SM postcodes. They also fail to account for the specialized materials needed for period homes, such as lime mortar or original sash windows, which can lead to a massive shortfall in your cover.

What happens if I don’t have an accurate RCA and I need to claim?

Your insurer will likely apply the “Average Clause” to your payout, which can be a financial catastrophe. If your reinstatement cost assessment for insurance reveals you are only covered for 70% of the true rebuild cost, the insurer will only pay 70% of any claim you make. This penalty applies even to small claims, meaning you would have to pay thousands of pounds out of your own pocket for repairs.

Does an RCA include the value of the land my house is on?

No, the value of the land is always excluded from the rebuild calculation. Since the land will still be there even if the house is destroyed, you don’t need to pay insurance premiums to cover its market value. The assessment focuses entirely on the costs associated with labor, materials, and the logistics of rebuilding the actual physical structure on that site.

Will my insurance premium go up if I get a professional assessment?

Your premium might change, but it will finally be accurate. If the survey shows you have been significantly underinsuring your property in Dartford, your premium may increase to reflect the true level of risk. However, since 27% of South East properties are currently overinsured, there is also a good chance your assessment could help you lower your premiums by removing unnecessary cover.

Do I need an RCA if I live in a flat in a larger block?

Generally, the freeholder or the management company is responsible for the buildings insurance for the entire block. You should check that they have an up to date RCA that reflects 2026 rebuild costs for the whole building. If you have carried out high end internal renovations to your flat in Greenwich, you must ensure these improvements are reflected in the overall sum insured for the block.

How long does the assessment take and when do I get the report?

A standard site inspection for a South London residential property usually takes between one and two hours. Our RICS-certified surveyors then analyze the data against the latest regional cost indices. You will typically receive your comprehensive and easy to understand report within three to five working days, giving you the clarity and confidence you need to secure your property.